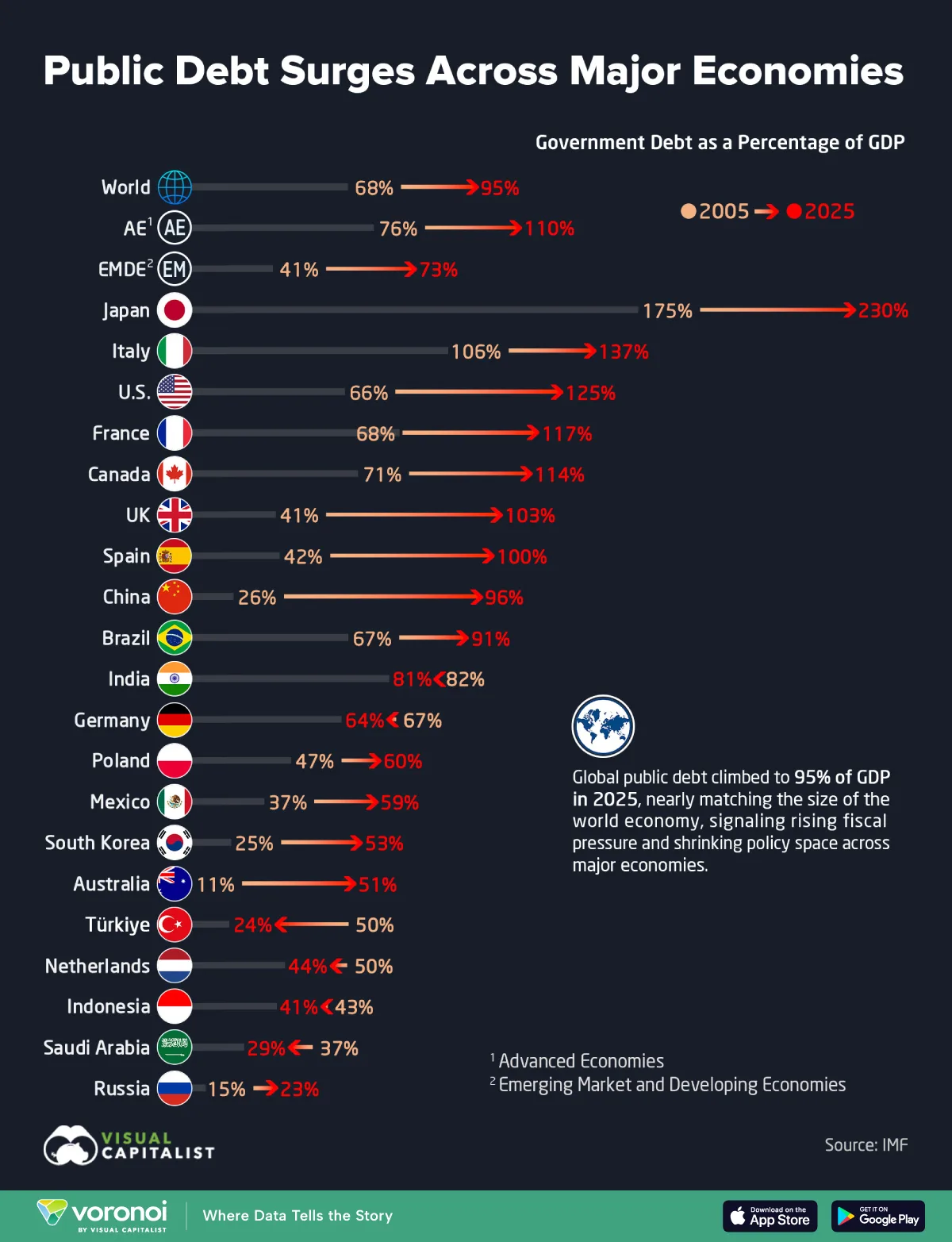

Global government debt has almost caught up with the size of the world economy, but the debt picture across countries remains uneven. Some developed countries have significantly increased their borrowing, while some developing countries, on the contrary, have been able to reduce their debt burden.

The world economy is entering a period in which government debt no longer looks like a temporary consequence of individual crises. For years, governments have been borrowing to cover deficits, finance social spending, anti-crisis programs, defense, and support the economy, and now the total amount of liabilities has almost equaled the size of world GDP. This figure hides a mixed picture: advanced economies have accumulated record debts, China has sharply increased its borrowing, and some developing countries have been able to reduce their debt burdens thanks to tighter fiscal policies.

In advanced economies, average government debt has risen from 76% to 110% of GDP, marking a shift from high but manageable debt to a level at which every rate hike or new crisis makes the budget much more vulnerable. Japan stands out the most, where debt is about 230% of GDP, more than twice the annual volume of the country’s economy. This figure has been maintained for years due to the peculiarities of the Japanese financial system, but it remains the highest among major advanced economies.

The United States, France, and the United Kingdom have also crossed the psychological threshold of 100% of GDP. American debt has reached about 125% of GDP, French debt — 117%, and British — 103%. For these economies, debt is not the result of a single decision, but rather a long-term combination of aging populations, high social obligations, budget deficits, and large-scale support programs during crises. The more expensive borrowing becomes, the more budgets are consumed by servicing old debts.

A similar trend has intensified in emerging market countries, although the starting positions there were much lower. The average debt in this group rose from 41% to 73% of GDP, with China showing the most notable jump, from 26% to 96% of GDP. This gap demonstrates how quickly debt financing has become part of the economic model of the world’s second-largest economy, which has actively supported growth through government spending and related liabilities.

Brazil and South Africa have also significantly increased their debt burdens, making them more dependent on the cost of credit and investor sentiment. The danger for such countries is not only in the percentage of debt to GDP, but also in their ability to regularly raise financing without sharply increasing the cost of borrowing. High rates quickly turn debt into a problem when a significant part of budget revenues goes to repay creditors.

Against this background, Turkey and Saudi Arabia look like exceptions, as they have managed to reduce their debt-to-GDP ratios. Their example shows that even in a period of global debt accumulation, countries can contain debt pressures by limiting deficits and implementing tighter fiscal policies. This path is politically difficult because it requires controlling spending, but it reduces a country’s dependence on creditors.

The International Monetary Fund expects global public debt to reach about 100% of global GDP by 2029. This level would be the highest since the post-war era, and the main sources of further debt growth are the United States and China. Additional pressure is created by high interest rates, increasing defense budgets, and geopolitical tensions, which are causing governments to spend more on security, industry, and strategic reserves.

The most acute part of the problem is that a debt of 100% of GDP for one country may be manageable, while for another, a much lower figure is already creating a crisis. Investor confidence, the structure of the debt, the currency of borrowing, the pace of economic growth, and the cost of servicing loans become decisive. As a result, dozens of countries, according to IMF estimates, are already in debt crisis or approaching it, although their figures may look more modest than the debts of rich economies.

Thus, world debt has almost caught up with the global economy, and this limit is becoming one of the main financial risks in the coming years. For strong economies, it means more expensive maintenance of government obligations, for weaker ones – the threat of spending cuts, currency pressure and dependence on foreign aid. That is why debt figures are no longer dry statistics: they show how expensive life on credit is for countries.